Reduce Capital Gains Tax on Property In New Budget by PTI Government

-

- June 13, 2020

- Pakistan Property News

- 0

New Budget by PTI Government to Reduce Capital Gains Tax on Property

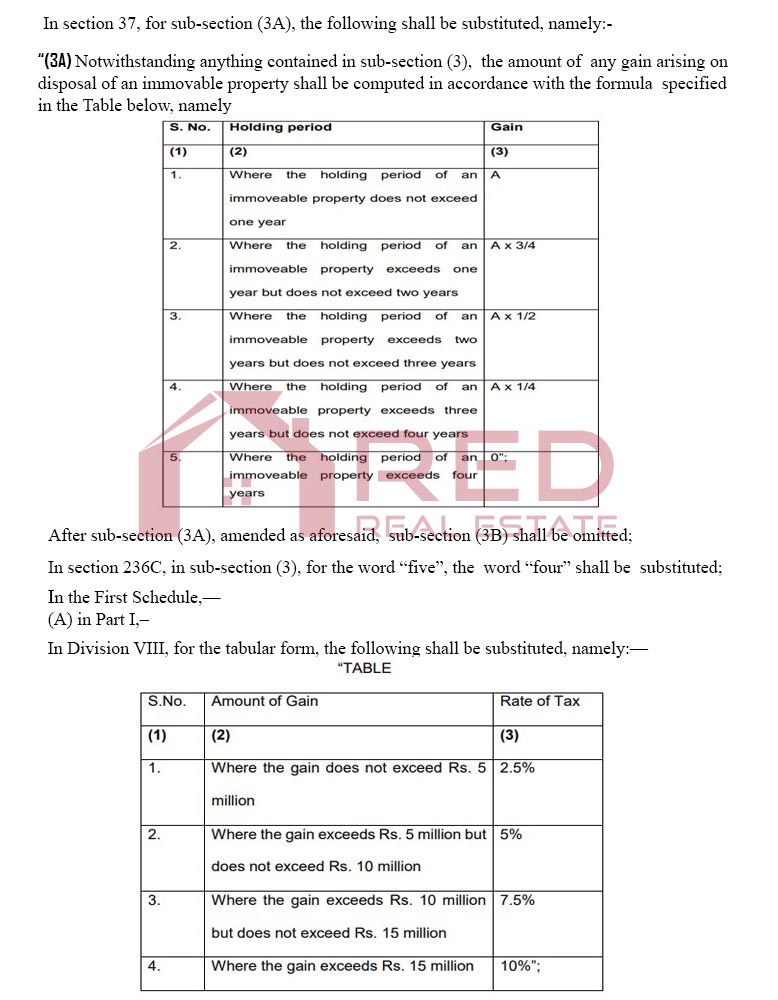

Despite what is included in sub-section 3, the amount of any profit arising from the disposal property should be calculated according to the formula specified in the table.

| Sr.No | Holding Period | Gain |

| (1) | (2) | (3) |

| 1 | Where the holding period of immovable property does not exceed one year | A |

| 2 | Where the holding period of an immovable property exceeds one year but does not exceed two years | A x 3/4 |

| 3 | Where the holding period of an immovable property exceed two years but does not exceed three years | A x 1/2 |

| 4 | Where the holding period of an immovable property exceeds three years but does not exceed four years | A x 1/4 |

| 5 | Where the holding period of an immovable property exceeds four years | 0 |

Capital Gains Tax on disposal of Immovable Property

| Sr.No | Amount Of Gain | Rate of Tax |

| (1) | (2) | (3) |

| 1 | Where the gain does not exceed Rs 5 million | 2.5% |

| 2 | Where the gain exceeds Rs 5 million but does not exceed Rs 10 million | 5% |

| 3 | Where the gain exceeds Rs 10 million but does not exceed Rs 15 million | 7.5% |

| 4 | Where the gain exceeds Rs 15 million | 10% |